Bond Prices Soar, Yields, Stocks Slump; Haven FX Outperform

2022-12-07 14:01:17

Risk-Off Heightens; AUD, CAD, EMFX Tumble, DXY Edges Up

Summary: Risk aversion ruled financial markets lifting bond prices and pushing yields lower. Wall Street stocks slumped. The dismal mood boosted the Dollar Index (DXY) higher to 105.55 (104.50).

The flight-to-quality lifted bond prices and pushed yields lower. At the close of trade in New York, the benchmark US 10-year treasury yield was at 3.53% (3.57% yesterday).

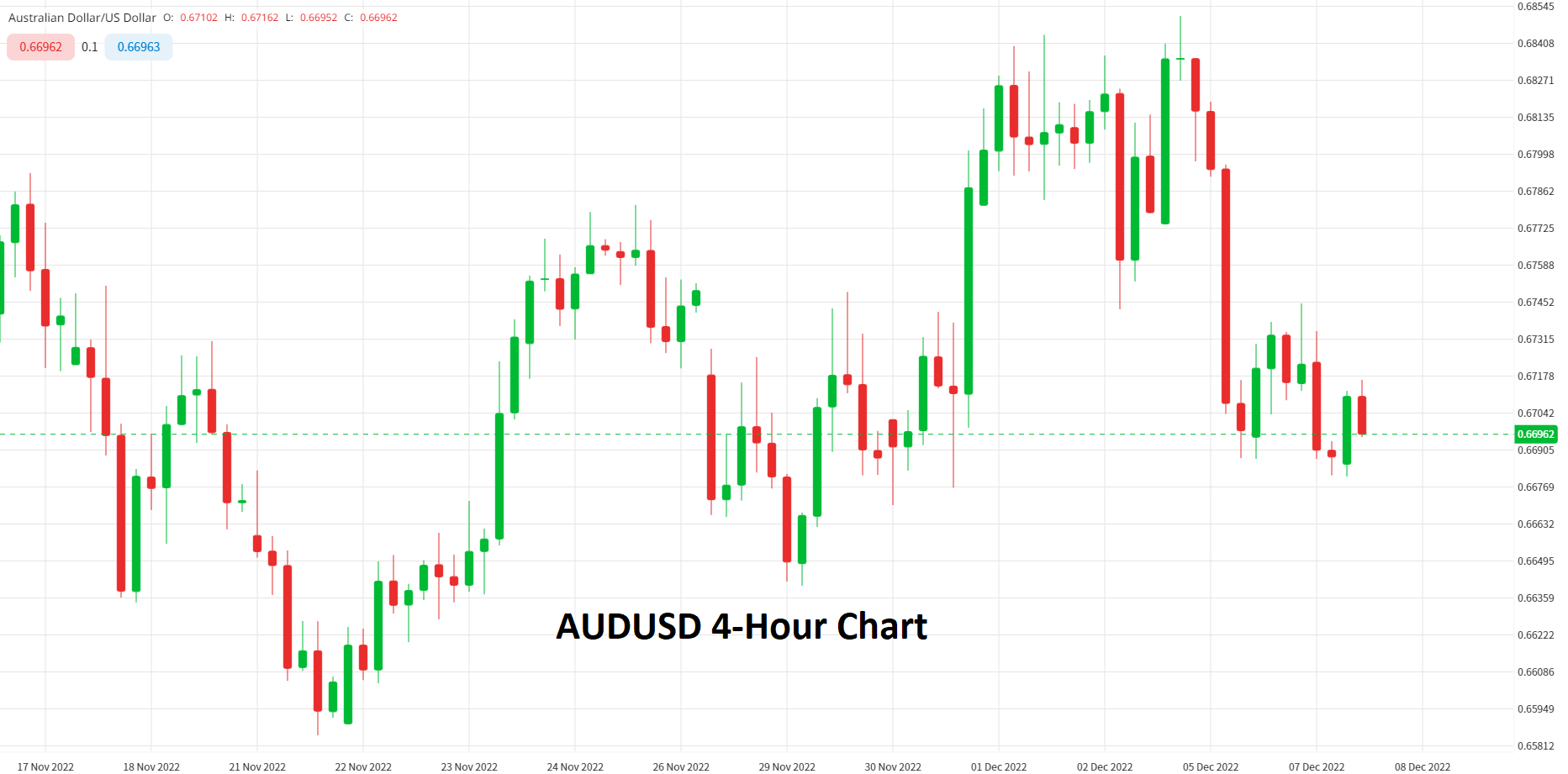

Resource and Emerging Market FX tumbled against the Greenback. The Aussie Dollar (AUD/USD) fell 0.3% to 0.6687 (0.6803) despite a 0.25 bps rate hike to 3.10% delivered by the RBA yesterday.

Against the Canadian Loonie, the Greenback (USD/CAD) rocketed to 1.3658 from 1.3475 on lower oil prices and risk aversion. The price of Brent Crude Oil slid 3.85% to USD 79.50 (USD 85.50).

The Greenback soared against the Thai Baht (USD/THB) to 35.07 (34.70). Against the Singapore Dollar (USD/SGD) rallied to 1.3595 from 1.3525 yesterday. Against China’s Offshore Yuan the US Dollar (USD/CNH) rose to 6.9845 against 6.9800 yesterday.

Sterling (GBP/USD) was pounded to 1.2140 from 1.2230. Data out of the UK saw November Construction PMI plunge to 50.4 from a previous 53.2, and lower than expectations at 52.0.

Despite a narrowing of yield differentials, the Greenback stayed firm against the Japanese Yen, (USD/JPY) rallying to 136.90 (135.00). At the close of trade in New York, the Euro (EUR/USD) slid 1.0465 from 1.0515.

Other economic data released yesterday saw German Factory Orders climb to 0.8%, beating median estimates at 0.2%. The US Trade Deficit eased to -USD 78.2 billion versus forecasts at -USD 80 billion.

Canada’s IVEY PMI climbed to 51.4 from a previous 50.1, better than median forecasts at 51.0.

- AUD/USD – the Australian Dollar tumbled to 0.6681 overnight lows (0.6803 yesterday) after the RBA lifted its Overnight Cash Rate to 3.10% from 2.85%. The move was widely expected, and the Aussie Battler settled at 0.6687 in late New York. Risk-off also weighed on the AUD.

- GBP/USD – after outperforming on Monday, Sterling reversed, tumbling lower against broad-based US Dollar strength to 1.2140 (1.2230 yesterday). Overnight high traded was at 1.2269 in another volatile trading session for the British currency.

- EUR/USD – the shared currency fell back to 1.0465 from 1.0532 following moderate gains earlier this week. Broad-based US Dollar strength and risk aversion weighed on the Euro. Overnight low traded was at 1.0460. ECB President Christine Lagarde is scheduled to speak on Thursday.

- USD/JPY – against the Japanese Yen, the US Dollar grinded higher to settle at 136.89 from 135.00. In volatile trade, the overnight high traded for the USD/JPY pair was at 137.43. An easing in US bond yields saw the Greenback edge back lower.

On the Lookout: Today’s economic calendar data dump kicked off earlier with Australia’s AIG Services Index for November which eased to 45.6 from a previous 47.7, missing median estimates at 48.6. The Aussie (AUD/USD) was unmoved, at 0.6690 following the report. Japan followed with its Reuters December Tankan Index which eased to 2 from a previous 3, and lower than median estimates at 3. The Reuters Tankan is a monthly survey of leading Japanese companies designed to provide early indications for the Bank of Japan quarterly tankan – ACY Finlogix.

Australia follows next with its Q3 GDP Growth Rate (q/q f/c 0.7% from a previous 0.9%; y/y f/c 6.3% from 3.6% - ACY Finlogix). Australia also releases its Final October Building Permits (m/m f/c -6% from -8.1% - ACY Finlogix). China follows with its November Balance of Trade (+USD 78.1 billion from a previous +USD 85.1 billion – ACY Finlogix); Exports (y/y f/c -3.5% from -0.3% - ACY Finlogix), November Imports (y/y f/c -6% from -0.7% - ACY Finlogix). Japan follows with its October Leading Economic Index (f/c 97 from 97.5 – ACY Finlogix). Switzerland starts off Europe with its November Unemployment Rate (f/c 1.9% from 1.9% - ACY Finlogix). Germany follows with its October Industrial Production (m/m f/c -0.6% from 0.6% - ACY Finlogix). The UK is next with its November Halifax House Price Index (m/m f/c -0.1% from -0.4%; y/y f/c 7.1% from 8.3% - ACY Finlogix). France releases its October Balance of Trade (f/c -EUR 16 billion from a previous -EUR 17.49 billion – ACY Finlogix). Italy follows with its October Retail Sales (m/m f/c -0.3% from 0.5%; y/y f/c 3.8% from 4.1% - ACY Finlogix)

The Eurozone is next with its Q3 GDP Growth Rate (q/q f/c 0.2% from 0.8%; y/y f/c 2.1% from 4.3% - ACY Finlogix), Eurozone Q3 Final Employment Change (q/q f/c 0.2% from 0.4%; y/y f/c 1.7% from 2.7% - ACY Finlogix). The US releases its Final Q3 Nonfarm Productivity (f/c 0.6% from -4.1% - ACY Finlogix). The Bank of Canada is widely expected to increase its Overnight Rate to 4.25% from 3.75%.

Trading Perspective: Expect markets to consolidate ahead of today’s data dump of economic reports. Rising risk aversion pushed the Dollar up against most of its rivals after falling this week.

Bond yields have moved more like spot FX and traders would do well to monitor them closely.

Resource and risk currencies have the most to lose in the current environment. Expect the Aussie, Kiwi, Canadian Loonie and Asian/EMFX to stay soft against the Greenback. And while yield differentials have lifted the US Dollar against the Yen, expect the Greenback to reverse if risk off extends. Volatility remained elevated as evidenced by the wide trading ranges in all currencies. We can expect more choppy trade today.

- AUD/USD – Expect the Aussie Battler to remain under pressure against the Greenback in the current risk averse environment. The AUD/USD pair closed at 0.6687. Overnight low traded was at 0.6681. Immediate support lies at 0.6680 and a break of that level will see 0.6650 tested. The next support level lies at 0.6620. Immediate resistance can be found at 0.6710, 0.6740 and 0.6770. Look for the Aussie to trade under pressure, likely range 0.6670-0.6730.

- USD/JPY – the Dollar stayed firm against the Japanese Yen despite a rise in risk aversion and a narrowing of yield differentials. The Greenback finished at 136.87 Yen. Immediate resistance today lies at 137.00 followed by 137.40. Immediate support is found at 136.60, 136.30 and 136.00. Look for further choppy trade in a likely range today of 136.30-137.30. Trade the range the best strategy for now.

- EUR/USD – the Euro slid back down against Greenback to 1.0465 from yesterday’s 1.0515. On the day, look for immediate support at 1.0460 followed by 1.0430 and 1.0400. Immediate resistance lies at 1.0500, 1.0530 and 1.0560. Look for the Euro to trade a likely range today of 1.0430-1.0530. Sell rallies.

- GBP/USD – against the strengthening Greenback, Sterling was pounded lower to a 1.2140 close from yesterday’s 1.2230. The overnight low traded was at 1.2137. For today, look for immediate support at 1.2110 followed by 1.2080 and 1.2050. On the topside, look for immediate resistance at 1.2170, 1.2210 and 1.2240. Look for further choppy trade in the British currency, likely range today, 1.2110-1.2240. Sell rallies.

Have a good Wednesday ahead all, happy trading.

This content may have been written by a third party. ACY makes no representation or warranty and assumes no liability as to the accuracy or completeness of the information provided, nor any loss arising from any investment based on a recommendation, forecast or other information supplied by any third-party. This content is information only, and does not constitute financial, investment or other advice on which you can rely.

延伸閱讀