NFP Breakdown June Employment: Cooling, Still Hot

2023-07-10 13:55:05

Summary

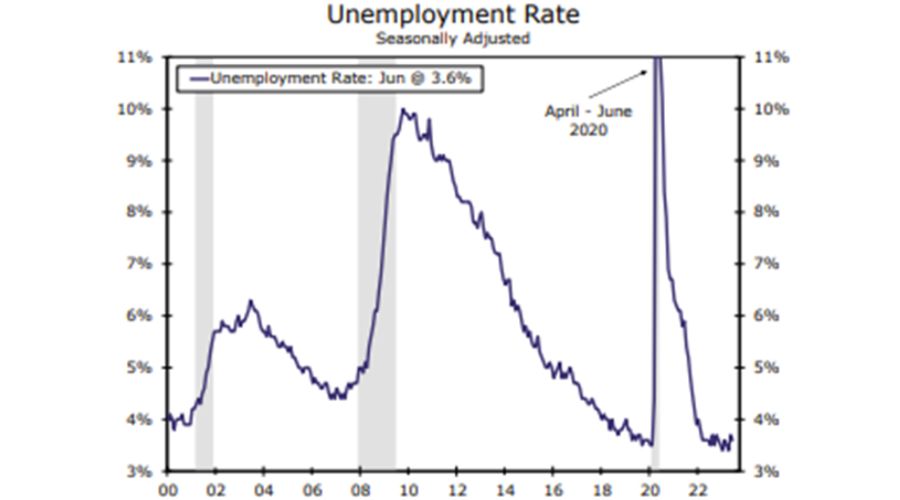

Nonfarm payrolls increased by 209K in June, coming in modestly below the Bloomberg consensus for the first time in 15 months. Downward revisions to job growth in the two previous months showed that employment growth has not been quite as strong as previously believed. Government hiring was once again robust (+60K), but the 149K increase in private sector employment was the smallest gain since 2020. The unemployment rate held steady at 3.6% and is unchanged from where it was in March 2022 when the FOMC hiked rates for the first time. Today's employment report offered additional evidence that the labour market is slowly coming into better balance as job growth slows and labour supply steadily expands. That said, job growth of +200K is still quite strong even if it is directionally slower than the scorching pace seen over the past year. A stronger-than-expected reading on average hourly earnings, as well as upward revisions to wage growth in earlier months, suggests the Federal Reserve is not out of the woods yet in its fight to tame elevated inflation. I expect a 25 bps rate hike from the FOMC at its upcoming meeting on July 25-26th.

Back to Earth for Payroll Gains

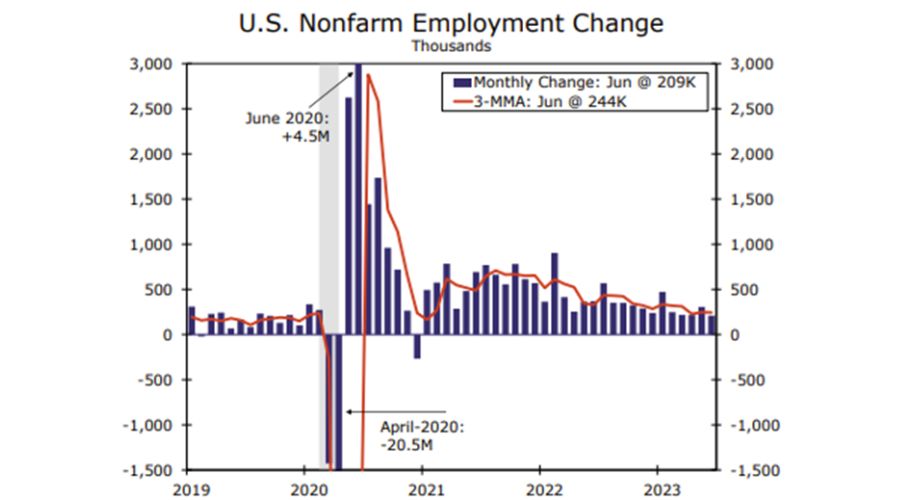

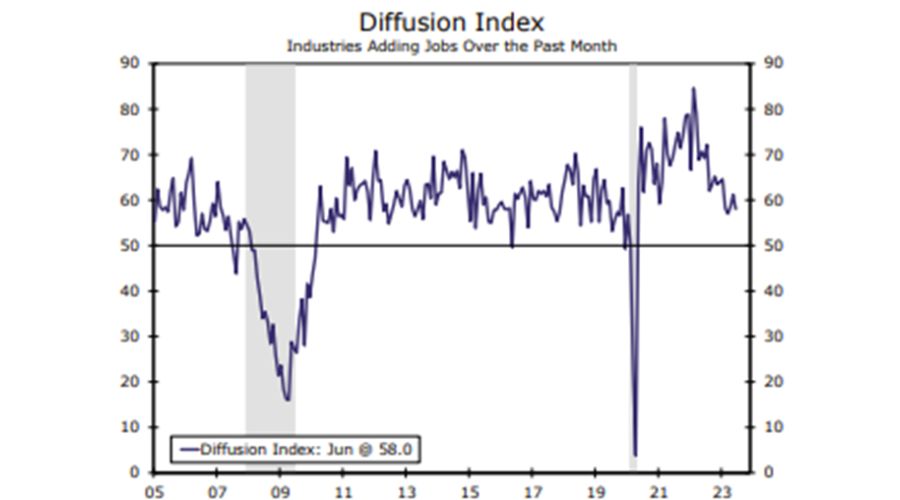

Nonfarm payrolls have seemed to defy the gravity weighing down other gauges of the labour market over the past year. However, the June employment report suggests this dynamic has run its course. Nonfarm payrolls increased by 209K in June—a respectable gain in its own right—but below the Bloomberg consensus for the first time in 15 months. Revisions also pointed to recent job growth flying a little closer to Earth. Payroll gains for April and May were revised down by a combined 110K, bringing the three-month average pace of job growth down to 244K. Job growth also narrowed a bit over the month with the diffusion index of industries adding jobs dipping to 58.0 from 61.2 in May. Government hiring was once again robust (+60K), but the 149K increase in private sector employment was the smallest gain since 2020. While the construction and manufacturing sectors posted solid gains, goods-adjacent services like retail, wholesaling and transportation & warehousing all saw employment slip over the month. Temporary employment also fell in June (-13K) in another sign that demand for workers is beginning to wane at the margin. After a sharp divergence between establishment-based payrolls and the household measure of employment in May, the two aligned more closely in June. Household employment rose by 273K, which outpaced another modest rise in the labour force (+133K) and helped drive the unemployment rate back down to 3.6%. The unemployment rate has remained within the narrow range of 3.4-3.7% since March of last year when FOMC began its most aggressive tightening campaign since the early 1980s.

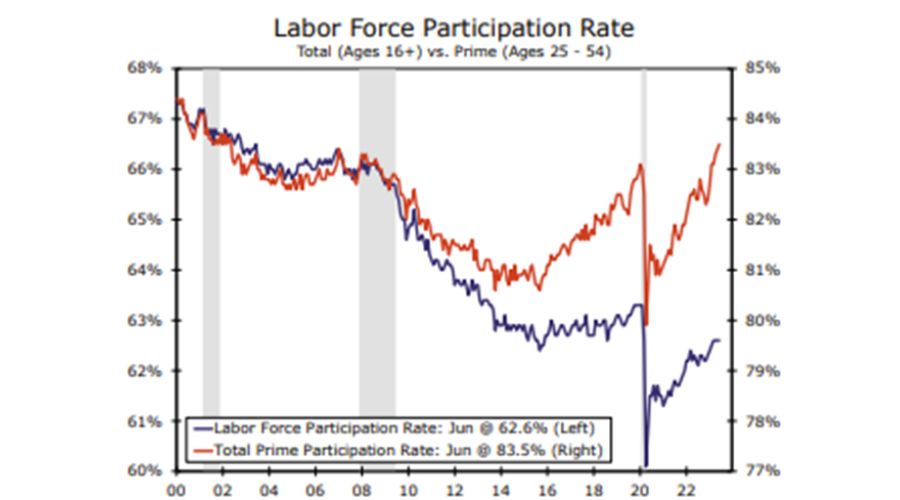

The labour force participation rate held steady in June at 62.6%, its fourth consecutive month at this level. A steady labour force participation rate is in some ways encouraging given that the aging population should put steady downward pressure on this measure over time, all else equal. The labour force participation rate for workers ages 25-54 ticked higher in June and is now at its highest point in more than 20 years (chart). After a sluggish start to the recovery, labour supply has expanded steadily over the past couple of years and should help bring labour supply and demand into better balance over time.

Wages Still Flying

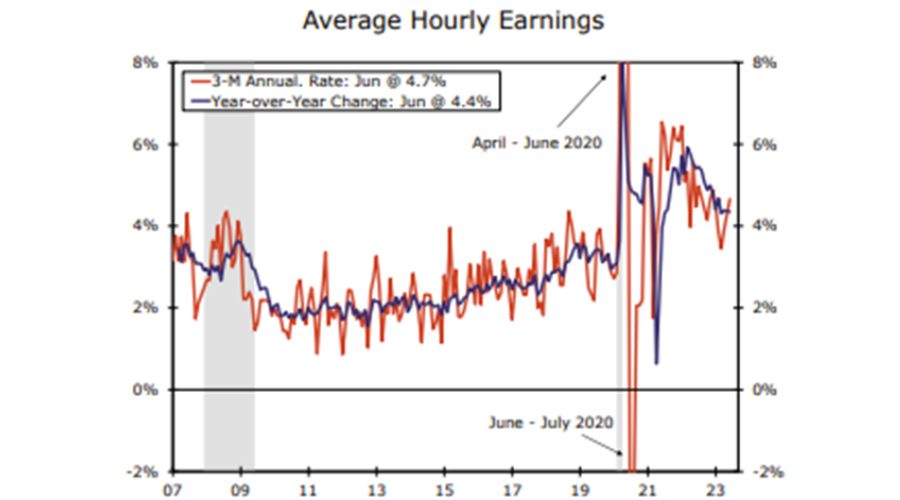

There had been signs of cooling wage growth in the recent monthly employment reports, but today's release partially dashed this disinflationary trend. The previous report showed average hourly earnings increasing at a 4.0% annualized rate over the three months ending in May, not too far off the ~3.5% pace that would be consistent with the FOMC's 2% inflation goal. Faster wage growth in June and upward revisions to the prior months pushed the three-month annualized rate up to 4.7%, above the year-ago rate of 4.4%. The Employment Cost Index report, to be released on July 28th, will provide a more comprehensive look at labour cost pressures in the second quarter. But based on what I know now, a tight labour market is keeping wage growth about a percentage point above what would be consistent with the FOMC's inflation target.

On balance, the labour market continues to cool, but only at a gradual pace. Through first half of the year, businesses added an average of 278K jobs per month, continuing a step down from 354K in the second half of 2022 and 445K in the first half of last year. That said, the directional slowdown has come off a scorching hot base, and +200K is still a very solid pace of job growth. Accordingly, the unemployment rate is no longer declining on trend, but it has yet to break higher. Jobless claims have inched higher, but they remain historically low along with the JOLTS measure of layoffs.

The surprisingly resilient labour market has helped to keep the U.S. economy expanding at a moderate pace despite continued fears about a recession. However, even amid more forthcoming labour supply and gradually cooling labour demand, the weight of the evidence still suggests that the labour market remains too tight to be consistent with 2% inflation. The directional progress towards a more balanced labour market is encouraging and helps explain why the FOMC has slowed the pace of its rate hikes, but last Friday data, point to another 25 bps rate hike at the upcoming FOMC meeting on July 25-26th.

This content may have been written by a third party. ACY makes no representation or warranty and assumes no liability as to the accuracy or completeness of the information provided, nor any loss arising from any investment based on a recommendation, forecast or other information supplied by any third-party. This content is information only, and does not constitute financial, investment or other advice on which you can rely.

ลองสิ่งเหล่านี้ถัดไป

4 Powerful Tactics to Overcome the Most Costly Forex Mistakes

How to Master MT4 & MT5 - Tips and Tricks for Traders

The Importance of Fundamental Analysis in Forex Trading

Forex Leverage Explained: Mastering Forex Leverage in Trading & Controlling Margin

The Importance of Liquidity in Forex: A Beginner's Guide

Close All Metatrader Script: Maximise Your Trading Efficiency and Reduce Stress

Best Currency Pairs To Trade in 2025

Forex Trading Hours: Finding the Best Times to Trade FX

MetaTrader Expert Advisor - The Benefits of Algorithmic Trading and Forex EAs

Top 5 Candlestick Trading Formations Every Trader Must Know