USDJPY: Is the USDJPY Heading for a Meltdown?

2026-04-22 14:40:07

Can the BoJ’s Hawkish Pause Hold the Line Against Increasing Oil price and Yields?

The pair yesterday with price opened at 158.799, closed at 159.376

The USD retains its dominance as the 10-year Treasury yield surge, driven by geopolitical friction.

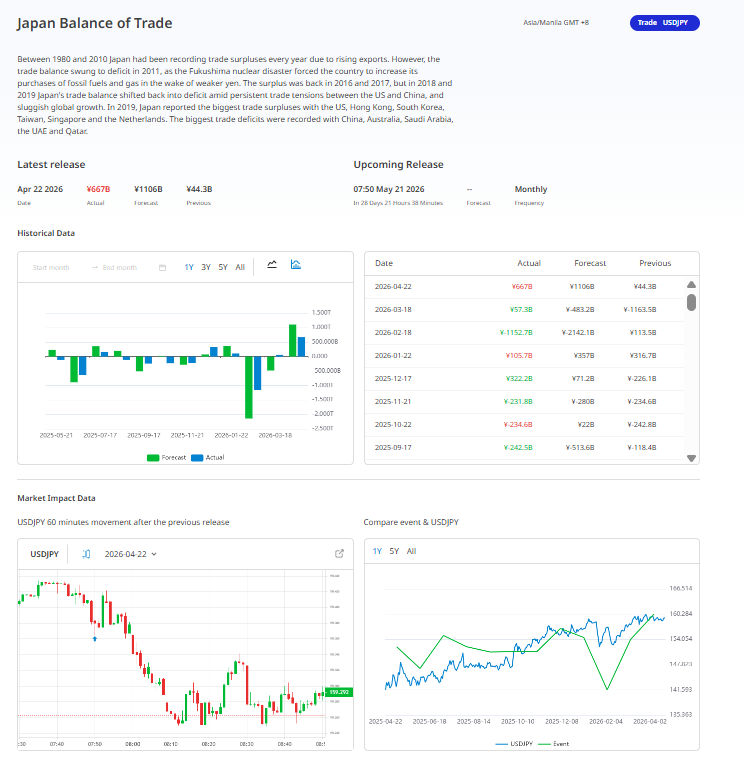

JAPAN BALANCE OF TRADE

The data from March or April 2026 shows Japan’s exports increased by 11.7%, and the trade surplus dropped by ¥667 billion well below the expectations at ¥1.1 trillion, due to a 10.9% rise in imports and driven by higher energy costs and supply chain disruptions impact from the Strait of Hormuz.

Since Japan is a net energy importer, increase in global oil prices weighing the Yen. U.S.

The U.S. continues to run a significant trade deficit (approximately $57.3 billion as of recent February/March prints), but the USD remains supported by high relative yields and its status as a haven during geopolitical tension.

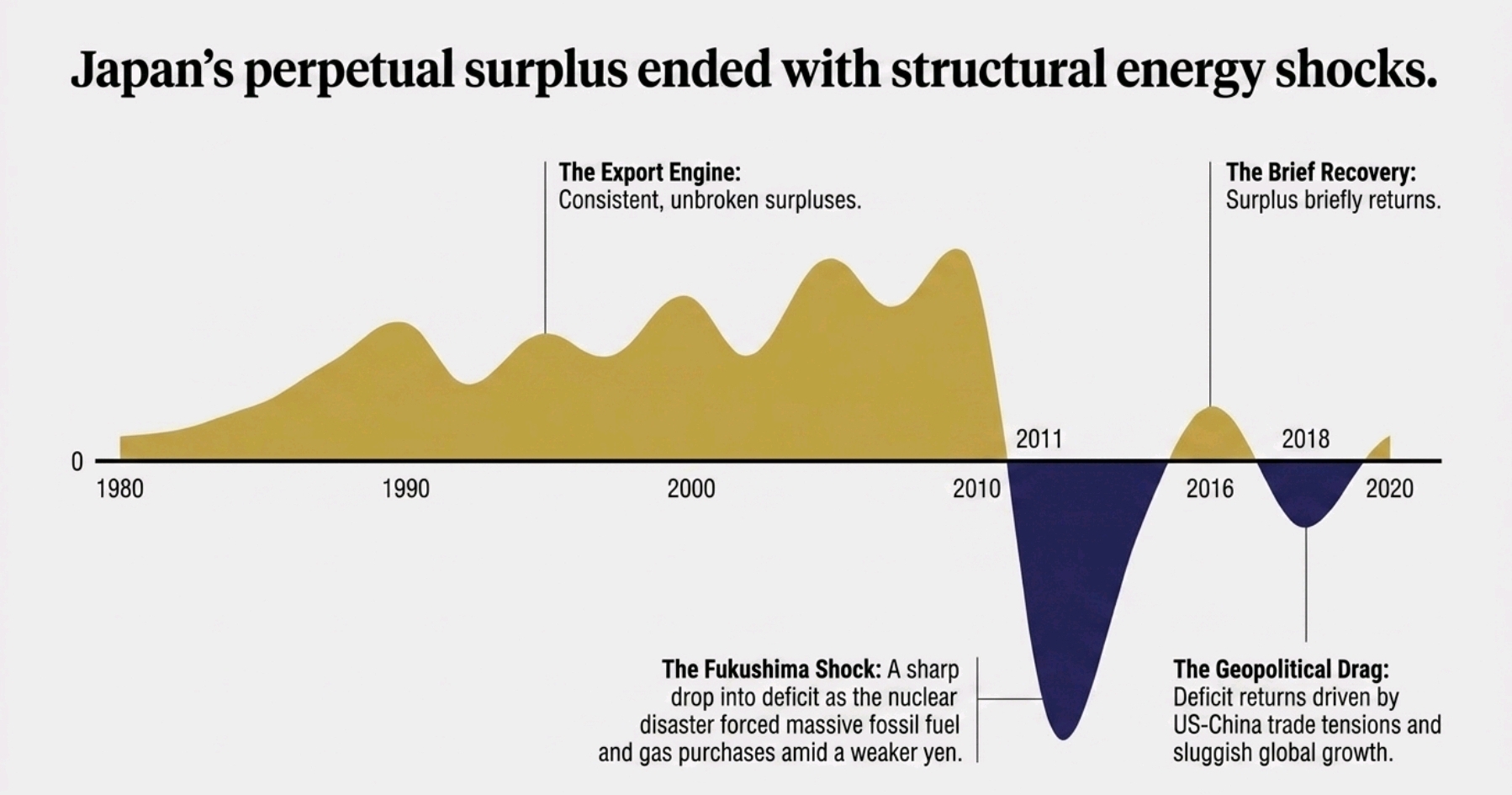

Japan Trade Dynamics & Structural Vulnerability

Long-Term Structural Shift: Japan's historical position as a dominant force in trade surpluses has given way to an environment marked by ongoing deficits. The energy traps a heightened susceptibility to global commodity prices made worse by a weak Yen that raises import costs is the main cause of this structural degradation, which is evident in the persistent negative prints throughout the 2024 to 2025 cycle.

Recent Performance (February/March Release): A notable exception to the bearish trend was the data that was made public on March 18. Japan posted an unexpected surplus of ¥57.3B, decisively defying the consensus estimate of a -¥483.2B deficit. While this beat was largely attributed to a temporary surge in external demand and seasonal export timing, it provided a brief respite for the Yen by slowing the pace of capital outflow.

SUMMARY

The core reason for the volatility of the pair is differences between the Federal Reserve and the Bank of Japan. In relevance to the Monetary Approach to the Exchange Rate, the relative supply and demand for money determine a currency's value. While the Bank of Japan’s cautious normalization maintains the Yen as the main financing currency for carry trades, the Fed's higher-for-longer posture (high interest rates) draws foreign capital seeking yield.

Japan’s Terms of Trade are currently under pressure due to its structural reliance on imported energy. In macroeconomic terms, when the cost of imports WTI Crude (West Texas Intermediate) rises faster than the value of exports, the Current Account suffers. This creates a mechanical Yen-selling requirement; Japanese importers must constantly sell JPY to purchase USD-denominated energy, creating a fundamental drag on the currency that persists regardless of technical chart patterns.

Leading Fundamental Indicators

- U.S. 10-Year Treasury Yields (US10Y) The Federal Reserve and the Bank of Japan have a nearly perfect positive connection with U.S. yields because of their wide interest rate gap. As capital flows seek the greater risk-adjusted returns of the dollar, Treasury rates rise and USD/JPY follows suit.

- WTI (West Texas Intermediate) Crude Oil Benchmarks.

U.S. Non-Farm Payrolls and Consumer Price Index are also key drivers for shift in Fed policy expectations.

Recent external drivers

Diplomatic Deadlines. The conclusion of the April 22 ceasefire and the status of peace talk regarding the Iran conflict are the primary wildcards for today's price movement. A breakdown in talks could trigger a risk-off flight to the Yen, potentially testing the 158.00 support level.

Updates from Bank of Japan

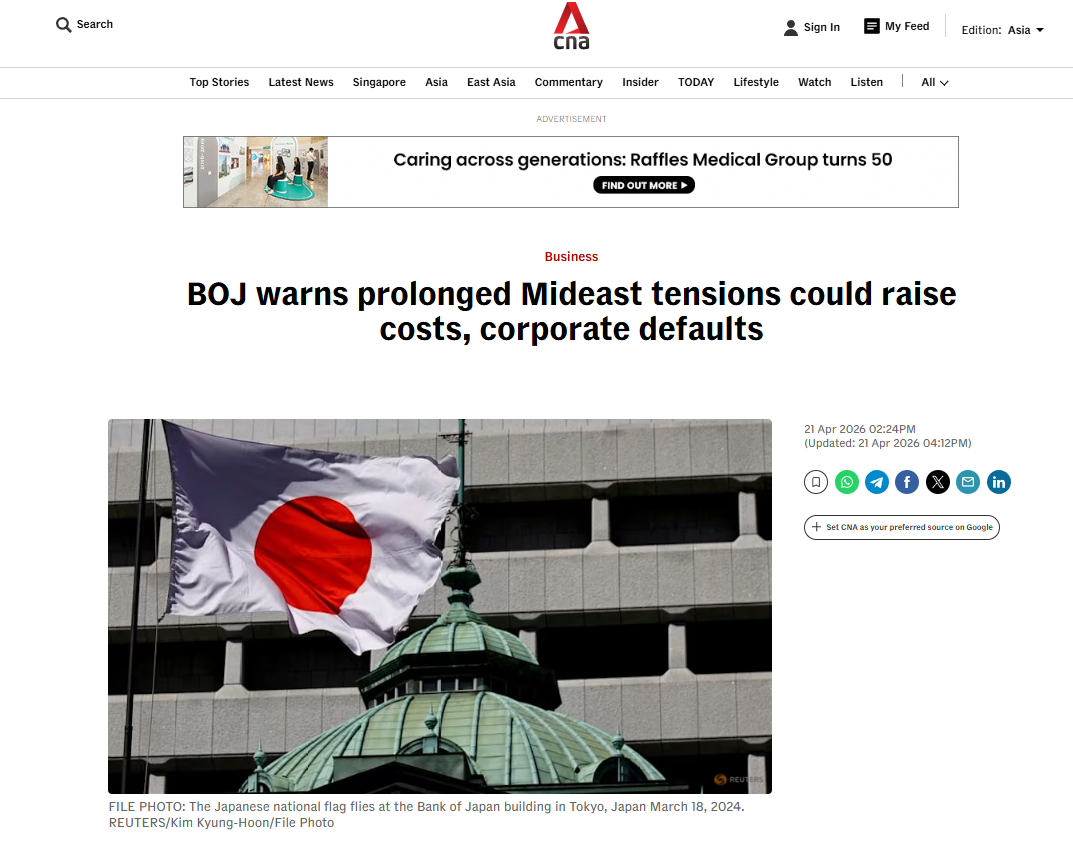

The Bank of Japan cautions that even while its financial system is solid right now, persistent tensions in the Middle East and rising energy costs could put a strain on company cash flows and increase the number of business bankruptcies. The research also draws attention to an increasing risk posed by the close ties between Japanese banks and international investment funds, which could hasten the transmission of financial stress from other countries into Japan.

Even though direct exposure is currently limited, the central bank is urging close monitoring of global market volatility to protect the country's financial resilience.

The Bank of Japan is to retain its rates on the upcoming meeting, as a defensive posture as Middle East volatility complicates the domestic recovery. Although increase in rate was previously suggested, policymakers now prioritizing with data-dependent evaluation to examine the cause of consistent energy price shocks on industrial output and consumer pricing. Despite the pause, the Bank of Japan is expected to keep up its hawkish posture, providing that a tightening measure is still visible in June to prevent further Yen depreciation. This conflict is likely to be reflected in the bank's upcoming quarterly report, which is expected to feature both lower GDP expectations and increased inflation forecasts because of rising gasoline prices.

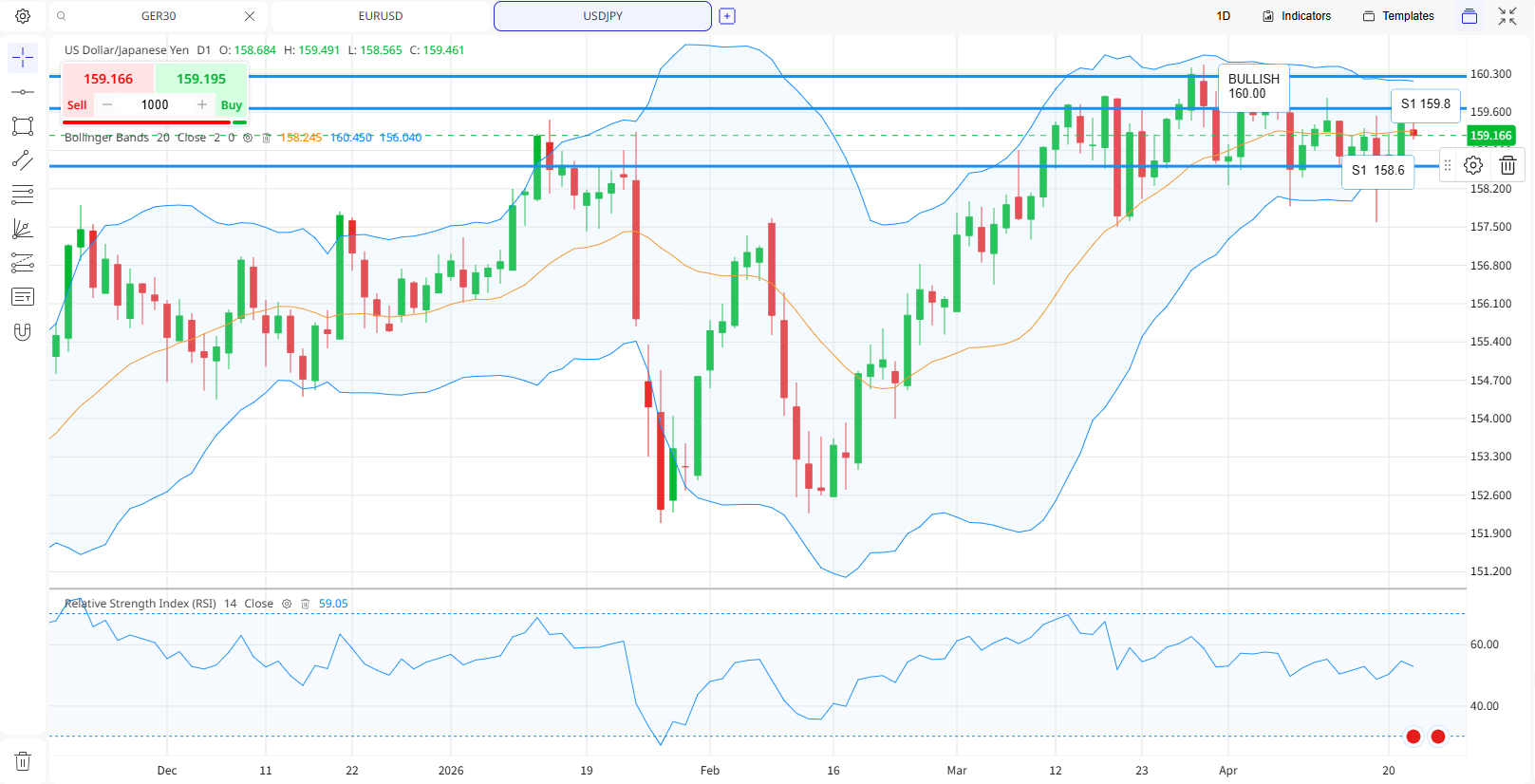

TECHNICALS

The pair is currently stagnant at 159.34 level within a broader ascending channel despite recent intraday volatility.

- Resistance 1 159.80 – if breached can drive to bullish signals

- Resistance 2 160.00 if breached

- Support 158.60 – 158.80 recent swing low support

- Relative Strength Index (RSI14) no overbought signals

Bank of Japan is providing a hold for the immediate April meeting due to uncertainty surrounding the Middle East conflict. Indicators for this year show inflation remain above the 2% target, leading markets to price in a potential rate hike in June. This hawkish pause is preventing a full breakout above 160.00 while providing a support price for the Yen against aggressive selling.

Conclusion & The ACY Edge

The current trend is bullish consolidation.

Disclaimer: This content may have been written by a third party. ACY makes no representation or warranty and assumes no liability as to the accuracy or completeness of the information provided, nor any loss arising from any investment based on a recommendation, forecast or other information supplies by any third-party. This content is information only, and does not constitute financial, investment or other advice on which you can rely.

Try These Next