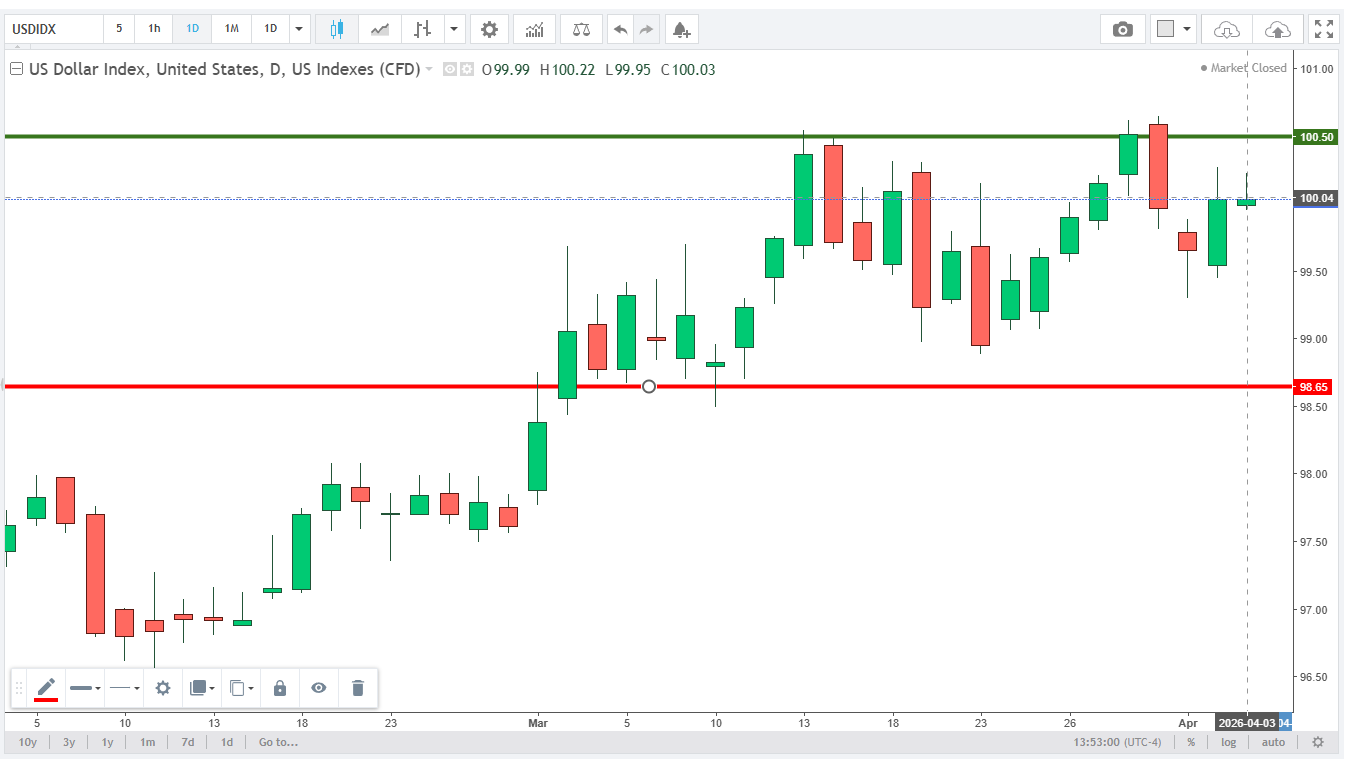

DXY at Crossroads: Will Global Conflict Push the Dollar Above 100.50?

2026-04-06 10:04:50

Is 100.50 the New Floor or a Ceiling for the Dollar Index?

The US Dollar Index (DXY) is currently locked in a stalemate between 100.00 and 100.50. While historical data typically suggests a seasonal softness for the Greenback in April, a powerful combination of geopolitical anxiety and energy shocks is acting as a massive anchor, keeping the index elevated against the trend.

The April decline typically stems from seasonal US tax obligations and a springtime surge in stock market optimism, reducing the overall demand for Greenback as a defensive asset.

Primary Market Drivers

Safe-Haven Pivot: Renewed tensions in the Middle East, specifically regarding potential infrastructure strikes, have forced investors to treat the Dollar as a primary hedge against global uncertainty.

The Energy Factor: With WTI Crude (West Texas Intermediate) crossing $110/barrel, fears of stagflation (stagnant growth mixed with rising prices) are mounting. This puts the Federal Reserve in a defensive position, inadvertently supporting the Dollar’s value.

Labor Market Caution: Traders remain sidelined ahead of the upcoming Non-Farm Payrolls. Any surprise hiring growth could provide the final spark needed for the US Dollar Index to punch through its current resistance.

Key Macroeconomic Benchmarks for the Week Ahead

To understand if the Dollar can maintain this strength, strategists must monitor these four performance pillars:

- Purchasing Managers' Index (PMI) A survey-based economic gauge that tracks the health of the manufacturing and service sectors; a reading above 50 indicates expansion, while a reading below 50 suggests a contraction.

- Core Inflation: A measure of price increases that excludes the often-unpredictable costs of food and energy to provide a clearer view of long-term, underlying inflation trends.

- FOMC (Federal Open Market Commitee) Mandate: The dual mandate given to the Federal Reserve to use its policy tools to promote maximum employment and maintain price stability, specifically aiming for a 2% annual inflation rate.

- Consumer Sentiment: An economic indicator that measures how optimistic or pessimistic people are regarding their financial security and the overall economy, which helps predict future levels of household spending.

Strategic Outlook: The Stalemate

The US Dollar Index is waiting for a definitive catalyst to break its current range. We are monitoring two critical levels:

Resistance (100.50): This is the ceiling. A clean break above this mark opens the door for a rally toward 102.00.

Support (98.65): This is the floor. A drop below this level would signal that the seasonal bearish trend has finally taken hold.

Conclusion & The ACY Edge

The global market is effectively on standby, paralyzed by the April 6 diplomatic deadline. This date represents the ultimate turning point for energy stability and investor confidence. Expect the Greenback to maintain this uneasy, volatile range until the outcome of these negotiations dictates whether the index breaks new highs or resumes its seasonal decline.

Disclaimer: This content may have been written by a third party. ACY makes no representation or warranty and assumes no liability as to the accuracy or completeness of the information provided, nor any loss arising from any investment based on a recommendation, forecast or other information supplies by any third-party. This content is information only, and does not constitute financial, investment or other advice on which you can rely.